You know all of those really important skills you should have learned in high school but never did? We’re talking about filing taxes, how to change a tire, and how to make a budget; actual life skills that most of us will use way more often than y=mx+b. Perhaps one of the most important topics that was left off of the curriculum was understanding a little thing called health insurance. If you feel like you’re way behind on this topic, you’ve come to the right place. Here’s your guide to understanding common health insurance phrases, where to get health insurance, and some important things to remember when it comes to using your benefits.

Terms You Should Know

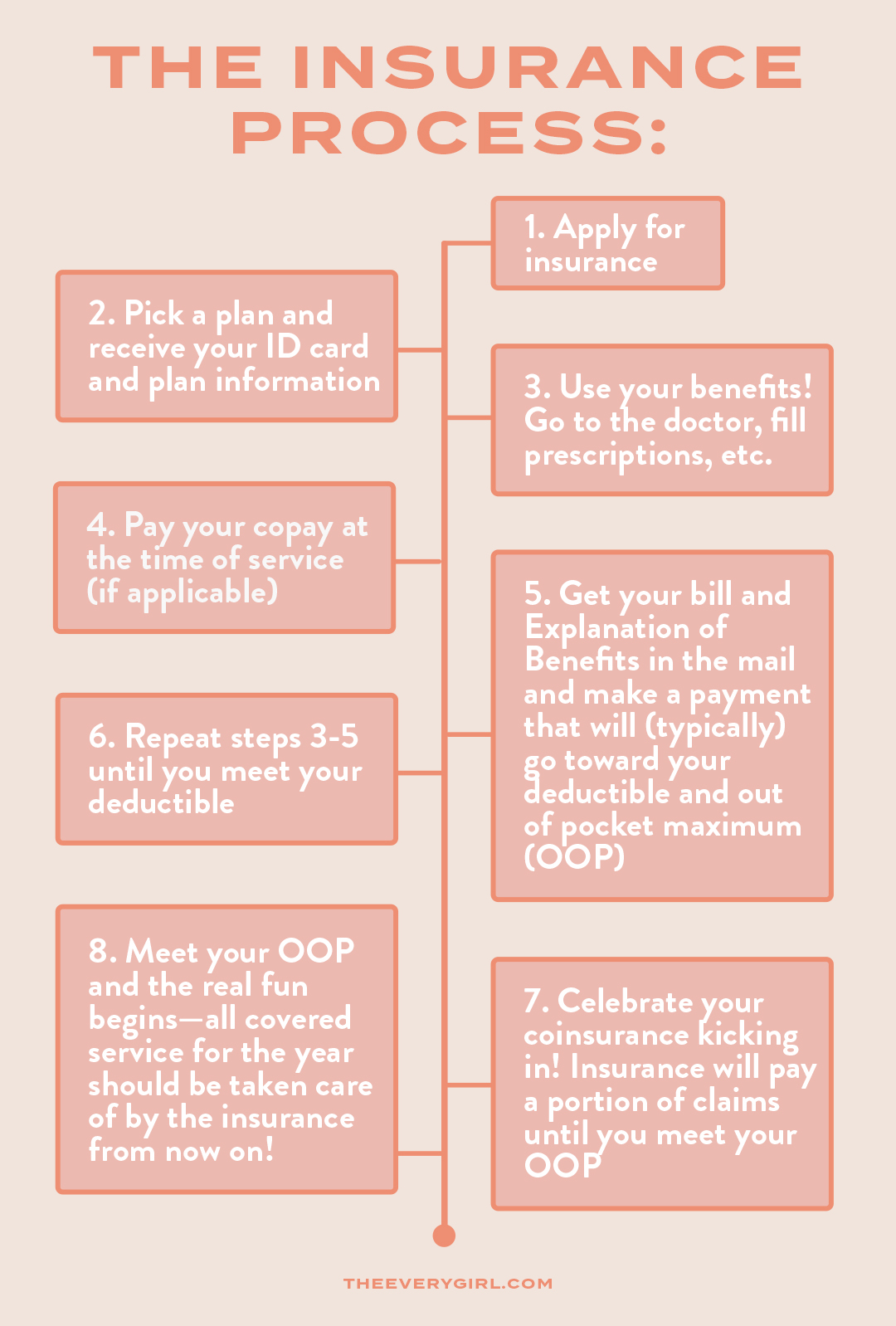

What’s a deductible?

Your deductible is the amount of money you will have to pay out of pocket in the year before the insurance benefits kick in. Think of your deductible as the points you have to rack up before you receive your next Abercrombie & Fitch reward. You spend x amount of dollars to get money off on your next purchase!

Your deductible can be anywhere from $0-$8,000, but in many cases will be in the $1,500-$4,500 range. To meet your deductible, you will use your health insurance card at doctor’s visits, to fill prescriptions, etc. You will then receive a bill from your doctor and what’s known as an Explanation of Benefits (or EOB) from your insurance carrier. This will show you that the claim from your visit was processed through the insurance and your payment went toward your deductible. Not quite as exciting as receiving your A&F package but still a positive nonetheless!

What’s coinsurance?

Once you meet your deductible, the insurance benefits begin. This is the percentage the insurance will pay toward a claim. This amount is generally between 50-100%. Let’s say your coinsurance is 70%. This means that, after you meet your deductible, the insurance plan will pay 70% of the claims that come in for covered services and you will pay 30%. For example, if you have a covered claim that is $100, the insurance will pay $70, and you will be responsible for $30. Isn’t it great having someone help out for a change?

What’s a copay?

A copay, or copayment, is a preselected amount that you will pay for certain benefits. Usually, you have a copay for prescription drugs, doctor’s office visits, and urgent care visits at the time of the visit.

Prescription drugs generally fall under 3-4 tiers, ranging from generic (or tier 1) drugs to specialty (tier 3 or 4) drugs. You may see prescription drug tiers such as $10/$65/$95/$200 or some variation of that.

Office and urgent care visits often also have set copayment amounts that you pay upfront. You may see $25 or $50 for office visits and $75 or $100 for urgent care.

Note: Not all health insurance plans utilize copayments. In this case, there will not necessarily be a set flat fee, and you will pay whatever the drug or office visit costs (bummer, we know).

What’s an out-of-pocket maximum?

Your out-of-pocket maximum (OOP) is the highest amount of money you will pay for covered services under your health plan for the year. If you reach your OOP, you can think of the rest of your health insurance benefits as “free” for the rest of the year.

The out-of-pocket maximum will generally include the deductible you previously met as well as any copays, but this can vary depending on your plan. From the example above, if coinsurance pays the $70, the $30 that you paid would go toward your out-of-pocket maximum. Once you’ve reached your out-of-pocket maximum for the year, all covered services going forward should be covered by insurance—completely, this time.

What are preventive benefits?

A majority of health insurance plans are mandated by the Affordable Care Act, meaning they will follow ACA guidelines for preventive benefits. These are the coveted services you generally get once per year, free of charge. Common preventive benefits include routine vaccinations, blood pressure screenings, cholesterol screenings, and more. You know, everything you need to stay in tip-top shape.

Preventive benefits are often split up between demographic groups. There will be certain benefits specifically for women, children, or all adults. Some benefits, such as colonoscopies, require you to be a certain age in order for the benefit to be considered preventive.

For a full list of preventive benefits, click here.

The Logistics

Where can I get health insurance?

Congratulations, you’re finally a true adult! Translation? You just turned 26 and are getting kicked off your parent’s health insurance plan. Now the real fun begins.

When this time comes, the most straightforward (and generally most affordable) way to obtain health insurance is through your employer. Many employers will pay a portion of your monthly premiums, contribute to a Health Savings Account for you, or (if you’re really lucky) offer free health insurance.

If you’re in the unlucky minority and can’t get insurance through an employer, you generally can enroll on a policy through the Marketplace/Exchange. All you have to do is meet all of the requirements, be able to afford it, sell your soul, and sign away your firstborn. Kidding!

As long as you meet all of the requirements, you can enroll in a marketplace plan on your own online, or you can reach out to an individual health insurance broker for assistance.

When can I apply for health insurance?

You’re going to want to get your insurance through an employer. When you begin a new job, you will generally have to go through a “waiting period” where you must work for the company for a set amount of time before you qualify to enroll on their insurance plan—this is typically anywhere from 0-90 days.

If you don’t enroll as a “new hire,” meaning within your waiting period, there may be limitations to when you can. Typically, you will need a Qualifying Life Event to occur, aka a big life-changing event like losing coverage elsewhere (example: adulthood/turning 26), getting married, having a baby, and more.

Generally, the only other time to enroll on a company’s health insurance plan is during their open enrollment period. Most companies renew their health insurance plans on Jan. 1, making their open enrollment period the month of December. This is the time period when employees who previously waived (or did not elect) the group health insurance plan are once again eligible and can enroll for a Jan. 1 effective date.

There are some cases when the insurance policy renews at a different time, making the open enrollment period different. Do your due diligence and check with your employer before taking our word as gospel.

If you are not seeking insurance through an employer and are looking at an individual or marketplace policy, you will likely have to wait for the annual open enrollment period or have a qualifying life event as well.

How much does health insurance cost?

Great question! We’d love to tell you, but the only answer here is that there is no one answer. Usually, the most affordable option is enrolling in a plan through your employer. Generally, the employer will pay a portion of your monthly premium. Your “premium” is the price you pay, generally monthly, to be enrolled on an insurance plan and have insurance benefits.

Not to be the bearer of bad news, but if you’re needing an individual health insurance plan, you’ll likely be responsible for paying the entire monthly premium yourself. Based on your demographics and the richness of the benefits you choose, this could range from $100-$400 monthly. Use those preventive benefits to stay as healthy as possible and keep costs down!

Things to Note

For some more good news, it’s important to remember that insurance doesn’t cover all medical procedures, as there are exclusions. Exclusions will be things like dental services, cosmetic procedures, alternative medicine, etc.

There is also a fun little thing called “pre-authorization” that the insurance company will often require before a major procedure. This means that your doctor must pre-authorize, or prove to the insurance company that the procedure is “medically necessary,” before they agree to cover the claim. This is something your provider’s office should be aware of, but we recommend trusting no one and taking it upon yourself to make sure this gets taken care of in advance.

Another thing to note is that deductibles, coinsurances, and out-of-pocket maximums are generally reset yearly. In many cases, this will happen on Jan. 1 each year, but there can be some variations.

Pro tip: If you are needing a service that will cause you to hit your deductible, schedule it toward the beginning of the year, or right after your plan resets, so your insurance benefits kick in and insurance pays a portion or all covered claims for the rest of the year. We DO NOT recommend taking this advice for anything that is life-threatening, of course.

If you have any questions regarding your health insurance benefits, what’s covered, or what you owe for covered services, bite the bullet and contact your health insurance company. Yes, you will likely have to wait on hold for an hour, but most companies now at least have the option for you to leave a message and receive a callback. This is one of those times it will be worth it to put in a little extra work, we promise